One of four millennials doesn’t think investing is a good idea.

Holding on to cash is financial hara-kiri.

The stock market isn’t out-of-reach and with a little amount, you can start investing.

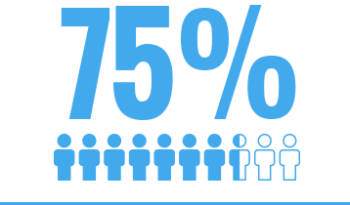

Millennials’ fears to invest in the stock market are shown in statistical data. Millennials are skeptical of the stock market at a great percentage. Yes, people! I can understand that. It isn’t easy to understand the stock market and when you don’t understand something, you are getting afraid. Moreover, you have heard a lot of scary stories. But take a look at your peers. Almost 1/4 think that a stock market is a great place to put their money. Are they braver than you?

Investing in the stock market has nothing to do with bravery it is all about common sense.

I know what you want to say: There are a lot of other ways of saving. Yes, that’s true. But is the return so great as with stock investing? Take a look at baby boomers! They stole cryptocurrencies from you, for example, not to mention other assets. Digital money should be yours. While you are hesitating to invest in the stock market, baby boomers and Gen X have an advantage.

Some of you may say: Yes, but they don’t have loans, they have homes, etc.

Sorry guys, but I have to disappoint you. They also have debts, mortgages, loans but don’t think the best way to earn more is to put cash in the savings account.

I’ll show you how wrong you are if you prefer to keep your cash in the savings account and how much you can lose over the years. Actually, I would like to show you how much you can earn if you invest in the stock market. So let’s make some comparisons.

Which are Millennials’ fears to invest?

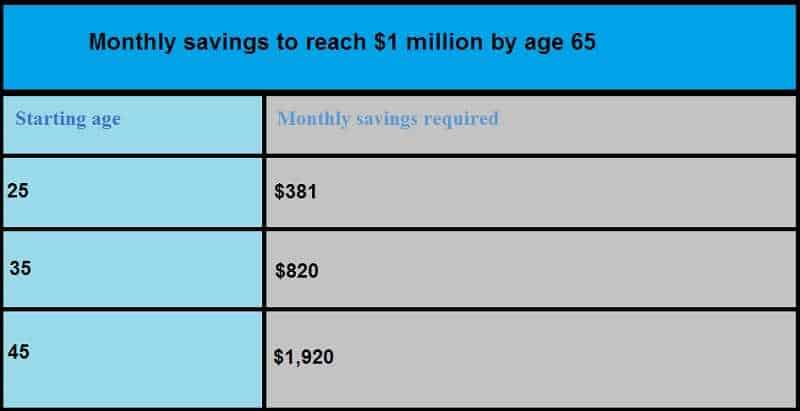

Do you really think you need a million dollars to retire? You’re going to be very discouraged. That amount isn’t even close to cover the cost of your bag of groceries. Inflation is what will make it tricky.

To put it simpler, your parents needed much less money to cover the cost of their bag of groceries when you were born. The costs increased by about 300% over the past 30 years. Scary! But you can’t destroy the inflation. Inflation is good for some things but it is another subject. Let’s stay stick with this one. Having this on your mind, are you still convinced that one million dollars is enough for your retirement? I am not sure. It is more like you will need more. By keeping your extra money on your savings account you will never earn enough to beat inflation.

Holding on to cash is financial hara-kiri.

If you don’t mind, I want to show you something.

Over the last 90 years, the returns of the S&P 500 was 10%. This is one example but the same is with other stock markets. How much your savings accounts pay you? Let’s say it is a high-saving one so you may have 1,5% per year.

Assume you have $50.000. If you put that amount on the savings account after 30 years you will have, without correcting for inflation, almost $80.000. This means your savings account could generate only $1.000 per year. But what would be your income if you invest your $50.000 in the stock market? After 30 years of investing in a nice portfolio, you could have almost one million dollars.

Can you notice the difference? Millennials’ fears to invest come from lack of knowledge about finances.

Why Millennials are afraid to put their money in the stock market?

Investing has never been easier, but millennials are still afraid to start investing.

You don’t need the fortune to get involved in the stock market. You are investing to make a fortune. Today we have online brokerages and robo-advisors. That makes investing pretty much easier than ever.

Further, data is easy to access. You don’t need to read newspapers to gather the info about some stock. Yes, sometimes it can be fun and may bring a lot of entertainment, who likes it. But you have plenty of other ways out there to find the stock. Data is now easy to access and usually totally free.

You can start at less than $1.000. No one will think you are a loser if you start with less than $1.000 or with just little as $100.

Take profit of this, and take command of your future.

Investing has never been easier

The stock market isn’t out-of-reach and with a little amount of, let’s say $500 you can start investing. That is an optimal amount that may provide you decently returns. Start with this, try your hand. Of course, for the first investment, you can use some robo-advisor.

Ask your bank advisor to create an investment portfolio for you. There is no need to do it yourself alone.

Millennials’ fears to invest are without a real reason. The money is like sand. If you squeeze it in your hand, it will go through your fingers.

Don’t do that. You can play better and become a real wealthy. Grab your chance to win!

The survey “War on Stress” showed young investors feel stressed and insecure while investing.

The survey “War on Stress” showed young investors feel stressed and insecure while investing.