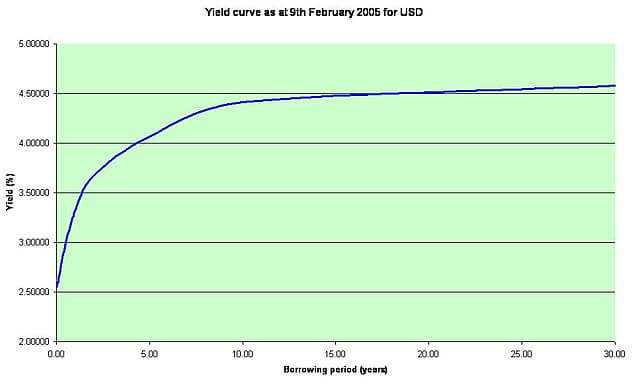

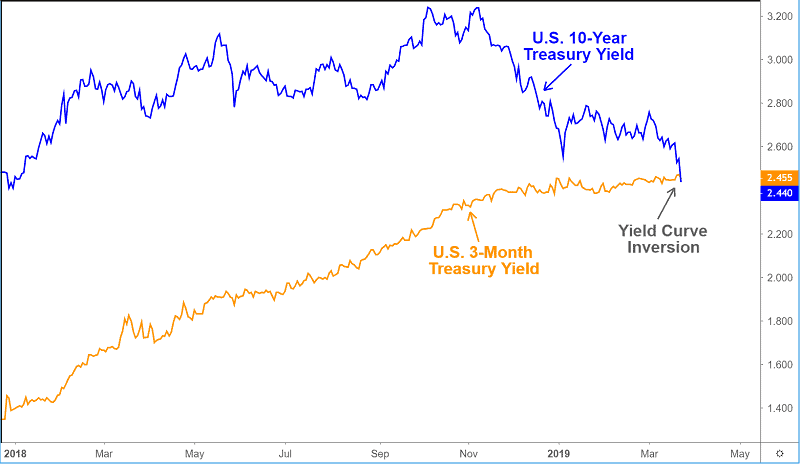

The yield curve, an indicator from the bond market a few months ago was inverted and started alerts about the risk of a recession. Yield curve turned positive now, and that brings relief to the markets.

The inverted yield curve is recognized as a recession warning. And now it isn’t inverted, the yield curve has turned positive now. So, can we speak about recession further? Well, that is not how these things work.

OK, the stocks are rising, but they have turned into the new high. And what investors have to do now, to wait or hop? It looks like investors are cautious.

The market is an all-time high, as a difference from the past two years.

The statistic is looking good for income investors since the 21 of the 30 Dow Jones Industrial stocks have yields of over 2%.

But a 10-year US Treasury bond yield is below 2%, that level seems to be too low. Therefore, there seems to be risk without a proper return from holding bonds now. This means, there is a reasonable expectation that investors could turn to stocks. When bond prices are low and yield is low, such as right now, the investors could move out of bonds into stocks because stocks are offering a better return now.

This is something known as great rotation.

The positive yield curve should be a sign that rationality has returned and the markets are in regular condition now. Are investors ready for this situation and are able to adjust immediately? We are afraid that changes happened too fast and investors couldn’t be efficient at making instant trades. Only a few months ago, investors were convinced that the recession is coming, since the yield curve was inverted. And now the inverted yield curve turned positive. Earnings reports are great, stocks are growing, consumer confidence is returning, conditions look excellent. How can we mention the recession anymore?

And this is something we have to make more clear.

The yield curve inversions virtually ever lead recessions, but it isn’t necessarily happening right now, in the same moment. What experts noticed is that we will need about 20 months or 2-3 months more or less to see the recession triggered by inversion of the yield curve.

What can we expect when the yield curve turned positive?

That should produce a change to the markets, and to forget a recession fears. This positive economic turn should produce stock prices to grow. How this can happen? Only if investors take action and invest. Their actions must have turned direction, they have to leave low yield bonds and jump into the stocks. So simple? Yes.

The truth is, we are in an atmosphere where even the smallest piece of negative news adds fears in our lives. When the negative yield curve appeared everyone was talking about it. The newspapers were reporting, the experts were screaming from TVs, investors moved to bonds. And what we had is that yield curve was inverted and now shifts very quickly to positive giving us no breath.

The stock market is driven by expectations but we all have to turn to reality. The reality is clear when it comes to investing: stay focused on long-term goals and avoid emotional reactions. Don’t pay attention to a daily stock price’s changes. We must have a bigger horizon.