Indian Forex market is not fully legal

Indian Forex market is not fully legal

By Guy Avtalyon

Forex trading in the Indian market is legal. RBI puts a lot of restrictions on trading, but still, there are possibilities for Indian residents to participate in the Forex market.

So, we can say, it is allowed to trade Forex inside Indian Exchanges. All resident Indian or companies, banks, and other financial organizations can trade in the currency market.

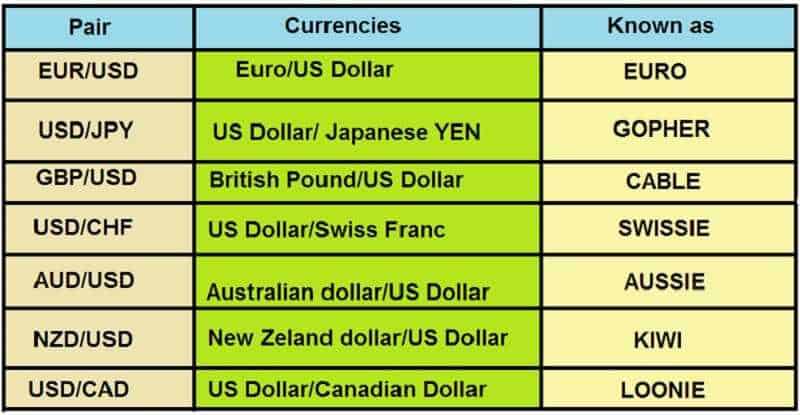

But Foreign Institutional Investors and Non-Resident Indians are not allowed to trade in the currency market. So, once again if you are resident Indian, you can trade currency over Indian exchanges like NSE, BSE, or MCX-SX. The main currency pairs are USDINR, EURINR, GBPINR, and JPYINR.

The point is that you can trade with respect to those two conditions: being resident Indian and the broker you choose is in the club of the exchanges mentioned above.

In those cases, Forex trading in India is unquestionably legal.

Forex trading in India is legal and safe.

There is remarkably strong regulation established by the RBI concerning Forex trading.

The problem is that RBIs regulation allows you to trade only 4 currency pairs, USD/INR, EUR/INR, GBP/INR, and JPY/INR.

But, it is possible to trade.

Yes, you cannot open an account out of the country, you have to trade with registered Indian brokers and listed currency pairs.

So, take this suggestion! If you are resident Indian and want to neglect the laws, you can also open an account using offshore exchanges. But you are doing that at your own risk.

Converting the INR to other currencies for the purpose of trading the FX markets with abroad Forex brokers is an illegitimate project. Such action in India is strictly against the law and can bring draconian penalties and also the prison.

How to do a Forex trading as an Indian trader

This is where things are a bit tricky. If you live in the rest of the globe, trading forex is the normal and regular thing.

For example, if you are a resident of some EU country or you live in the US, you can trade any currency pair in the world. You can trade even over unregulated brokers, at your risk of course. But when you trade on Forex market that is pretty unregulated you are trading at your risk anyway.

When it occurs in India, it is quite complex.

Is Forex trading fully legal in India

The problem is that trading currencies in Forex trading in the Indian market is not fully legal.

You have only one possibility, and it is the same for the resident Indian, you can trade only the currency pairs that have INR (Indian Rupee). And you may choose among 4 currency pairs USD/INR, EUR/INR, GBP/INR, and JPY/INR.

What is the story behind this? We assume one possible scenario. The US dollar is the most popular and the most traded currency.

And INRs value in comparison with the US dollar is too low. So, if many traders would like to buy dollars, the Central Bank of India could be short. The next what the Central Bank of India could do is to buy dollars. But the price would not be the same. It could be much much higher. It is possible at worse rates and INR will continue going down.

That sounds logical.

In the same way, online trading and using online platforms are not allowed for Indian citizens. Foreign brokers can offer their services in Forex trading in the Indian market. Though, Indian traders can trade only with brokers certified by SEBI. And again, they can trade only currency pairs denominated in INR.

This the moment when we have to say that it would be smart to reconsider those limits. In such a case, Indian Forex traders could enjoy full currency trading.

As we heard and read several times, the Indian government is contemplating eliminating the restrictions in order to provide the other popular pairs to be traded. That will be nice.

Until then, if you want to trade with abroad brokers, you should be sure that they have the required licenses.

Our recommendation is to choose the approved Forex broker that has an extraordinary credit. It isn’t hard to find some, for example, TradeO.

Trading Platforms for Forex trading in the Indian market

For Indian traders, it is impossible to use online Forex platforms or software. Simply, it is illegal.

But still, not all Indian traders are citizens of India, so they can use them.

For those who can trade online from India, there are few things to consider.

Choose the broker with a user-friendly interface.

Also, it has to easy to manipulate.

The button that can close all of your positions when you want that has to be included and visible.

Further, your broker must offer you several platforms. One, for example, Metatrader 4 or Metatrader 5, that you can download and at least one to trade from your browser.

The most convenient is if you choose the broker that provides you to download the app. You can easily install it on your phone.

So, you don’t have to be stick to one place when you want to trade.

When it comes to account types, the majority of brokers will allow you to open the account with a small deposit. It can be, for example, $50-$100.

But maybe you want to trade with a much bigger amount of money. Anyway, you should contact your chosen broker and discuss the rules, and find out which type of account suits you best.

Also, you should check if your broker has a free demo account. Either you are an advanced or beginner trader. Trading on a free demo account will give you the view of how the platform works, or you can learn more before you give them your money.

Happy trading, India!

Here are Traders-Paradise’s suggestions for the automated trading software we examined.

Here are Traders-Paradise’s suggestions for the automated trading software we examined.

Start investing with $100 only is possible, here is how to do that.

Start investing with $100 only is possible, here is how to do that.

Real estate investing is easiest to understand but getting started can appear scary

Real estate investing is easiest to understand but getting started can appear scary