DEFINITION of Adverse Excursion

Adverse Excursion is the loss attributable to price movement against the position in any one trade.

WHAT IT IS IN ESSENCE

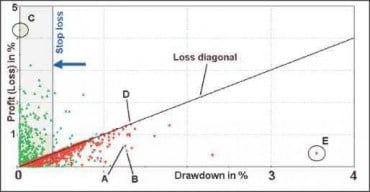

In order to find proper stop points for your system, you should take a deeper look into the distribution of trades. Also, examine each trade individually. When you do so, you will discover that there are similarities between them. But that every trade also has its own set of characteristics.

These characteristics can be examined by using this loss. It is defined as the most intraday price movement against your position. In other words, it’s the lowest open equity during the lifespan of a trade.

This concept allows you to evaluate your systems’ individual trades. Of course, in order to determine at what percentage amount or currency to place your protective stop.

There are two types of Excursions: Maximum Favorable Excursion (MFE) and the MAE Maximum Adverse Excursion (MAE).

The MFE marks the highest price during a long trade and the lowest price during a short trade. This shows you what the highest profit was during a trade.

The MAE is one of the metrics that is produced by most backtesting systems. It measures the largest loss suffered by a single trade while it is open. For example, a trade may end up closing at a profit of, say, 14 points. But while that trade was open, at one point, the trade was at a loss of 13 points. Assuming that no other trade was in such a losing position during the backtesting then this would be the MAE.

HOW TO USE

For example, if XYZ shares were bought for $500 each and the share has fallen to $400. The adverse excursion would be $100 or the degree to which the trade is “out-of-the-money”. A strict stop-loss strategy would prevent adverse excursion from becoming too large as a proportion of the original investment. The term is more commonly used in the derivatives market.