Traders-Paradise

Developing Trading Algorithms

Free members enjoy complimentary access to all featured bots.

Premium members receive exclusive benefits, including access to put/short trades.

Subscribe now at $27/month for advanced trading strategies and insights, or join free to get these features:

Community Engagement

Members can engage in discussions, share insights, and collaborate with like-minded individuals, creating a supportive environment for learning and networking

Live Trading Opportunities

We provide real-time trading alerts, notifying users of potential trading opportunities as they happen

Stock Analysis Tools

Unlock elite trading analysis tools and insights for free – no sign-up required!

Auto Stop Trailing Alerts

Enjoy the perks of our automated stop trailing alert system. Set your trailing stops, and let the system monitor stock prices. Receive notifications when a stop is reached – all automated, and it’s completely free of charge and automated.

Membership Access

Members gain access to more exclusive features.

For traders seeking advanced features, our membership provides exclusive access to short trades and put trades. Enjoy complimentary access to long positions – our way of empowering your trading journey..

Free for Beginners

For those starting their trading journey, our platform is entirely free! Advanced traders seeking hedge options for their trades will find a specialized service available at a charge

Seamless Trading, Expert Insights

At Traders-Paradise.com, we’ve engineered an intuitive private Discord server.

Blending advanced technology with user-friendly interfaces.

Our real-time data processing and smart algorithms provide unique trading prospects.

Technological Trade Companion

Elevate your trades with Traders-Paradise Bot! Key indicators, detailed charts, and timely alerts for a guided trading experience.

Interactive Trading Assistant

Elevate your trading experience with tp-bot! Auto Stop Alerts, stock comparisons, and a game-changing Macro Feature. Empower your decisions with evolving features. Join now!

Ultimate Research Tool

Unlock your trading journey’s full potential with OpenBB Bot! Dive into stocks, options, cryptos, and more. Explore 120+ features, stay ahead with real-time insights. Elevate your strategies now!

Unveiling the Secrets Behind Our Bots

Unlock the potential of algorithmic trading!

Explore the inner workings of our Discord bots in this ‘How It Works’ video:

Stock: PH | Date: 2022-03-16 | Entry: $304.36 | Exit: $324.36 | Profit: +6.5%

Stock: PH | Date: 2022-03-16 | Entry: $304.36 | Exit: $324.36 | Profit: +6.5% Stock: PARA | Date: 2022-03-24 | Entry: $20 | Exit: $22.4 | Profit: +10%

Stock: PARA | Date: 2022-03-24 | Entry: $20 | Exit: $22.4 | Profit: +10% Stock: AEM | Date: 2022-03-21 | Entry: $49.2 | Exit: $51.8 | Profit: +5.6%

Stock: AEM | Date: 2022-03-21 | Entry: $49.2 | Exit: $51.8 | Profit: +5.6% Stock: LUMN | Date: 2022-03-30 | Entry: $2.56 | Exit: $2.67 | Profit: +5%

Stock: LUMN | Date: 2022-03-30 | Entry: $2.56 | Exit: $2.67 | Profit: +5% Stock: TU | Two successful trades, one in November, one in March

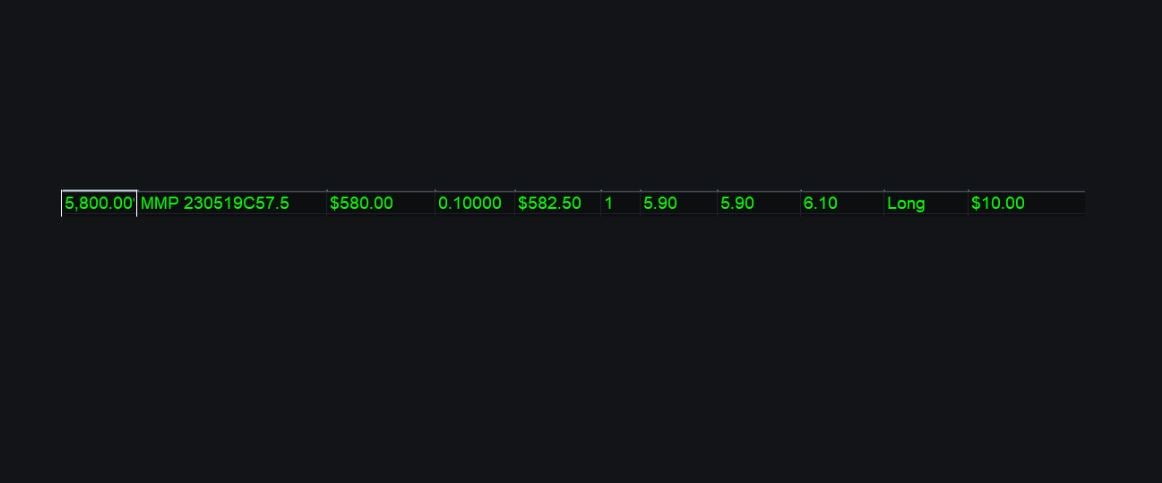

Stock: TU | Two successful trades, one in November, one in March Stock: MMP | 2023-05-10 | Entry: $10 | Exit: $580 | Profit: +5,800% (OPTION)

Stock: MMP | 2023-05-10 | Entry: $10 | Exit: $580 | Profit: +5,800% (OPTION) Stock: BALL | 2023-05-02 | Entry: $85 | Exit: $530 | Profit: +535% (OPTION)

Stock: BALL | 2023-05-02 | Entry: $85 | Exit: $530 | Profit: +535% (OPTION)